Thursday 12 June: Fabrice Lumineau (HKU)

Add to Calendar Apple Google Office 365 Outlook Yahoo The architecture of interfirm illegality: how...

Thursday 15 May: Irina Surdu (Warwick)

Add to Calendar Apple Google Office 365 Outlook Yahoo Is (s)he worth it? Behavioural agency, CEO...

Thursday 10 April: Ana Aranda (UvA)

Add to Calendar Apple Google Office 365 Outlook Yahoo Legal Resonance: How Restrictive Laws Shape...

Thursday 13 March: Hyejun Kim (HEC)

Add to Calendar Apple Google Office 365 Outlook Yahoo Knitting Community: Human and Social Capital in...

Thursday 13 February: Anne Jacqueminet (ESSEC)

Environmental disclosure and analysts' recommendations About the Research This paper investigates how...

Thursday 9 January: Romain Boulongne (IESE)

Embedded in unrest: The paradox of embeddedness in the wake of nascent social movements About the Research...

Thursday 5 December: Panikos Georgallis (UvA)

Assembling the market puzzle: Social movements, opportunity configurations, and market formation About the...

Thursday 7 November: Patrick Haack (UNIL)

Unveiling Propriety, Validity, and Consensus: A multilevel examination of legitimacy following the Global...

Thursday 10 October: Yuliya Snihur (IESE)

Unlocking social impact at scale: The power of entrepreneurial framing About the Research We study how a...

Tuesday (Not Thursday!) 25 June: Yuan LI (Saint Mary’s College of California)

From latency to salience to knotting: A dynamic disequilibrium model of paradox management About the...

Thursday 13 June: Anne-Claire Pache (ESSEC)

Orchestrating multiple actors for social innovation: the role of common grounding About the Research...

Thursday 16 May: Mario Amore (HEC Paris)

Time tells: Unraveling the temporal and risk dynamics of venture capitalists About the Research Access...

Thursday 14 March: Saverio Favaron (SKEMA)

The experts and the crowd: The interplay between qualified rankings and consumer ratings About the...

Thursday 15 February: Francesco Castellaneta (SKEMA)

Hybrid entrepreneurship and wage dynamics About the Research Using matched employer-employee data from...

Thursday 11 January: Anders Krabbe (King’s College)

From Revolution to Revenue Stream: How Corporate Targets Co-opt Social Movement Attacks About the...

Monday 18 December: Fabien Accominotti (UW-Madison)

Meritocratically Unequal: How the Reification of Merit Hierarchies Fuels Inequality About the Research...

Tuesday 5 December: Olenka Kacperczyk (LBS)

STORM & The Entrepreneurship and Innovation Research Center Proudly Present: Gender Gap in Startup...

Thursday 9 November: Farah Kodeih (IESEG)

Building collective resilience in times of rising authoritarianism: Civil society organizations in Orbán’s...

Thursday 12 October: Ilze Kivleniece (INSEAD)

Leviathan as a client: Public vs private contracting of desalination technologies to address water scarcity...

Tuesday 30 May: Elisabeth Clemens (U. of Chicago)

STORM & The Entrepreneurship and Innovation Research Center Proudly Present: Beyond efficiency and...

Thursday 4 May: Emanuele Bettinazzi (USI Lugano)

How do categories influence target selection in corporate acquisitions? About the Research In the M&A...

Thursday 13 April: Elisa Operti (ESSEC)

Taking on the Mob: How Multinational Enterprises Navigate Institutional Uncertainty in Organized Crime...

Thursday 9 February: Brayden King (Northwestern University)

Environmental Protests, Shareholder Activism, and the Struggle for Corporate Autonomy. About the Research...

Thursday 12 January: Madeline Toubiana (University of Ottawa)

Sexy work not sex work: Craft creation as a mechanism of destigmatization. About the Research Workers in...

Thursday 15 December: Marjo Siltaoja (University of Jyväskylä)

What counts in moral markets: Categorical salience and moral evaluation in German carsharing markets. About...

Thursday 17 November: Shaz Ansari (Cambridge University)

Navigating nascent platform legitimacy: A framework for the dynamic deployment of framing strategies. About...

Thursday 20 October: Maxim Voronov (York University, Canada)

When work is everything: Coping with institutionalized perfectionism About the Research Perfectionism is...

Thursday 16 June: Dror Etzion (McGill University)

Generative research for addressing societal grand challenges: The case of the PIVOT project About the Research...

Thursday 12 May: Tieying Yu (Boston College)

The power of words: Word responses in multimarket competition About the Research Previous research has...

14 April 2022: Jan Lodge (Erasmus University)

Sustaining compassion as central organizational competence About the Research In this study, we explore how...

10 March 2022 – STORM Insights in Quant methods: Olga Novoselova (emlyon)

STORM Insights in Quant methods: Estimating the relative importance of predictors: research questions, study design, and analytical tools.

14 March 2022: Zeke Hernandez (Wharton)

Does Employing Skilled Immigrants Enhance Competitive Performance? Evidence from European Football Clubs About...

10 February 2022: NUNO OLIVEIRA (Tilburg)

Power and Trust in Interorganizational Relationships

13 January 2022: Johanna Mair (Hertie School)

Varieties of Alternative Organizing: Novelty and Conventionality in Organizing around Social Problems

16 December 2021: Joel Gehman (George Washington University)

Remaking capitalism: The strength of weak legislation in mobilizing certification

2 December 2021 – STORM Insights in Quant methods: CLEMENT LEVALLOIS (emlyon)

STORM Insights in Quant methods: Explore textual data without coding

18 November, 2021: ABHINAV GUPTA (University of Washington)

Stakeholder Ideological Incongruence and Diffusion of Controversial Practices: Evidence from LGBT Domestic Partner Benefits Adoptions by U.S. public universities

21 October, 2021: DAPHNE DEMETRY (McGill University)

Divergent Myths: Occupational Change in the Culinary Industry

24 June, 2021: GIADA DI STEFANO (Bocconi)

To Stem the Tide: Organizational Climate and the Locus of Knowledge Transfer

27 May, 2021: ANNA KIM (McGill U.)

Cui Bono? Organizational Legitimacy and Social Impact in Corporate-Community Relations in Kenya

29 April, 2021: JUNG-HOON HAN (U. of Missouri)

Public enemies? Reputation and celebrity as interpretive frames in the scandalizing of organizational misconduct

25 March, 2021: GRACE AUGUSTINE (City U)

Have you tried this? Co-constructing and accessing a repertoire of implementation for moral mandates

25 February 2021: JELENA BRANKOVIC & LEOPOLD RINGEL (Bielefeld University)

Theorizing Rankings: A Sociological Approach

28 January 2021: CAROLINE FLAMMER (Boston U.)

"STORM Proudly Presents" Seminar Series: Caroline Flammer (Boston U.)

"Impact Investing and the Fostering of Business Ventures' Financial Performance and Social Impact in Disadvantaged Urban Areas"

4 June 2020: AMANDINE ODY-BRASIER (Yale)

Accounting for Negative Attention: Status and Costs in the Market for Audit Services

CANCELLED: 12 March 2020: OLIVER HAHL (Carnegie Mellon)

Can Faking it Lead to Making it: The effect of industry scandal on symbolic and substantive organizational change

How a relational database can help you manage your data: Introduction to SQLite.

How a relational database can help you manage your data: Introduction to SQLite.

19 December 2019: MASSIMO MAORET (IESE)

Is there a Symbolic Effect of Social Status on Performance? Exploring Causal Evidence and Underlying Mechanisms

28 November 2019: GINO CATTANI (NYU)

Overcoming the liability of novelty: The power of framing

24 October 2019: PASCUAL BERRONE (IESE)

A behavioral perspective of search in nonprofit organizations: How programmatic aspirations drive fundraising efforts

26 September 2019: MITALI BANERJEE (HEC Paris)

Who Becomes Famous Among Creative Pioneers? A Large-Scale Empirical Study of the Relationship Between Novelty and Fame Across Time and Space

20 June 2019: CHARLENE ZIETSMA (PennState)

The Microfoundations of Belief and Behavior Change: A Field Experiment on the Efficacy of Frame Bridging and Frame Shifting Strategies for Stimulating Innovative Entrepreneurship

BrainSTORM: our new workshop series for early-stage research

We’re delighted to introduce our new workshop series, BrainSTORM. BrainSTORM is intended for presentations of...

16 May 2019: NOAH ASKIN (INSEAD)

Is There a Gender Gap in the Novelty of Creative Products? Evidence From the Global Music Industry, 1955–2000

11 April 2019: FREDERIC GODART (HEC)

Mobility Networks and Institutional Change: How Parisian Haute Couture Moved into Ready-to-Wear, 1945-1973

11 March 2019: ERIC ZHAO (Indiana U.)

Optimal Distinctiveness in CSR Practices: Examining the CSR Profile Extensiveness and Deviation among Chinese Publicly Listed Companies

14 February 2019: ISABEL FERNANDEZ-MATEO (LBS)

Gender Differences in Reapplication after Rejection and Women’s Representation in Talent Pipelines

17 January 2019: NILANJANA DUTT (Bocconi)

Complex Learning: Evidence from U.S. Manufacturing

13 December 2018: BRYANT HUDSON (IESEG)

Collective Rage, Power, and Institutions: Examining the Processes of Institutional Disruption, Defense and Reaction

15 November 2018: MAJKEN SCHULTZ (Copenhagen Business School)

When Strategy Needs Identity and Vice Versa: A Temporal View of the Strategy-Identity Interplay

18 October 2018: JULIANE REINECKE (King’s Business School)

From Symbolic Commitment to "Skin in the Game": Collective Action and Institutional Formation through Problem Solving

27 September 2018: KAMAL MUNIR (U. of Cambridge)

From Patañjali to the Gospel of Sweat: Yoga's Remarkable Transformation into a Multi-Billion Dollar Market

25 June 2018: RAGHU GARUD (PennState U.)

Generative Imitation, Strategic Distancing and Optimal Distinctiveness During the Growth, Decline and Stabilization of Silicon Alley

15 June 2018: AMELIA COMPAGNI (Bocconi U.)

Veiling and unveiling the membership of the Sicilian Mafia (1963-2016): Struggles, strategies and set-backs

31 May 2018: CHRISTIAN DE COCK (CBS) & DANIEL NYBERG (Newcastle)

Disrupting Climate Change Denialism in Management and Organization Studies

26 April 2018: TAL SIMONS (Tilburg U.)

The Construction of Authenticity in the Creative Process: Lessons from Innovative Choreographers of Contemporary Dance

22 March 2018: JOHN AMIS (U. of Edinburgh)

Image, Emotion, and the Framing of the European Migration Crisis The European migration crisis has become one...

08 March 2018: STINE GRODAL (Boston U.)

Big, Beige and Bulky: Æsthetic Shifts in the Hearing Aid Industry (1945-2015) Æsthetics play an important role...

01 March 2018: EMILIE FELDMAN (Wharton, U. Penn)

Two Sides of the Same Coin: Family Firms and the Performance of Acquisitions and Divestitures

15 February 2018: GIOVANNI VALENTINI (IESE)

Discrimination and Entrepreneurship: Evidence from LGBT Rights Laws

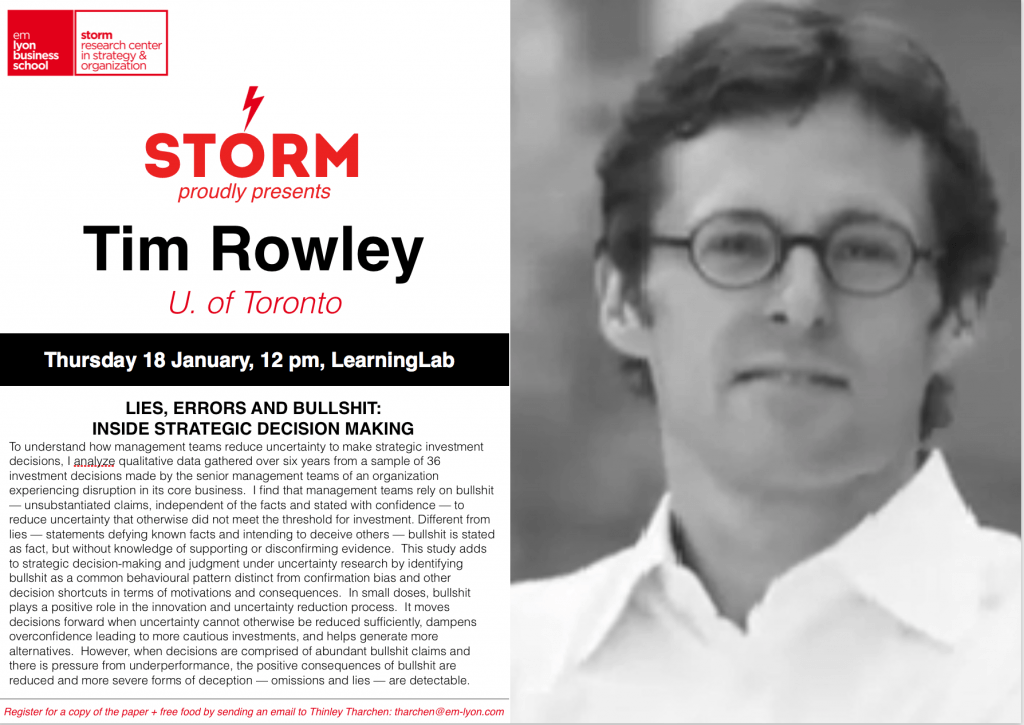

18 January 2018: TIM ROWLEY (U. of Toronto)

Lies, Errors and Bullshit: Inside Strategic Decision Making

30 November 2017: JULIEN JOURDAN (U. Paris-Dauphine)

Social valuation across multiple audiences: The interplay between ability and identity judgments

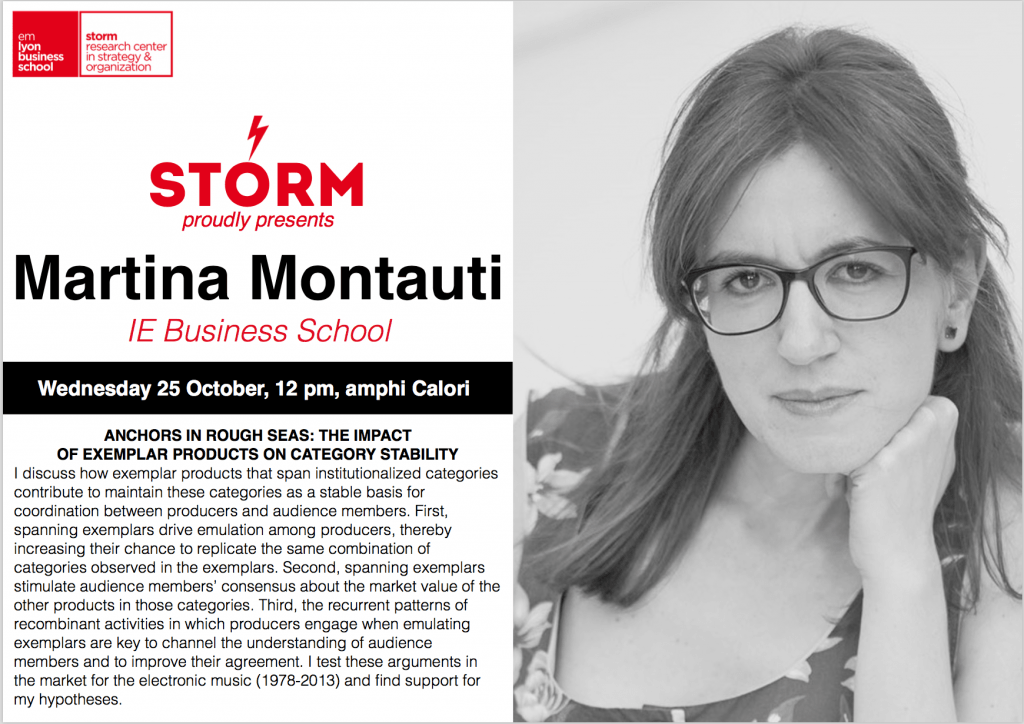

25 October 2017: MARTINA MONTAUTI (IE Business School)

Anchors in Rough Seas: The Impact of Exemplar Products on Category Stability

11 May 2017: STOYAN SGOUREV (ESSEC)

Rivalry Flips the Script: Gender Effects in Network Recall and Activation (with Elisa Operti and Shemuel Y....

09 February 2017: TAMMAR ZILBER (Hebrew U. of Jerusalem)

Institutional logics on the ground

08 December 2016: RENATE E. MEYER (WU Wien)

Towards a structural model of institutional pluralism In this talk I combine institutional theory with...

08 December 2016: ROY SUDDABY (University of Victoria)

The professionalization of the corporate historian The corporate historian/archivist is a relatively recent...

10 November 2016: STEFAN JONSSON (Uppsala University)

Segregating Competition In this talk, I draw on Hirschman’s (1970) Exit, Voice, and Loyalty to investigate the...